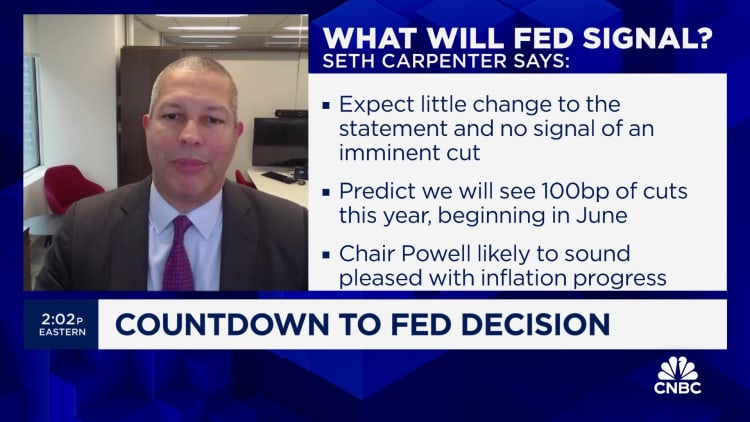

The Federal Reserve announced Wednesday it will leave interest rates unchanged, setting the stage for rate cuts to come and paving the way for relief from the combination of higher rates and inflation that have hit consumers particularly hard.

Although Fed officials indicated as many as three cuts coming this year, the pace that they trim interest rates is going to be much slower than the pace at which they hiked, according to Greg McBride, chief financial analyst at Bankrate.

“Interest rates took the elevator going up; they are going to take the stairs coming down,” he said.

More from Personal Finance:

Forget a soft landing, there may be ‘no landing’

‘Positive’ labor market data can feel awful. Here’s why

Gen Z is getting money advice from TikTok

Inflation has been a persistent problem since the Covid-19 pandemic, when price increases soared to their highest levels since the early 1980s. The Fed responded with a series of interest rate hikes that took its benchmark rate to its highest in more than 22 years.

The federal funds rate, which is set by the U.S. central bank, is the interest rate at which banks borrow and lend to one another overnight. Although that’s not the rate consumers pay, the Fed’s moves still affect the borrowing and savings rates they see every day.

The spike in interest rates caused most consumer borrowing costs to skyrocket, putting many households under pressure.

Below the surface, 60% of households are living paycheck to paycheck.

Greg McBride

chief financial analyst at Bankrate

“Below the surface, 60% of households are living paycheck to paycheck,” McBride said. Even as inflation eases, high prices continue to strain budgets and credit card debt continues to rise, he added.

Now, with rate cuts on the horizon, consumers will see some of their borrowing costs come down as well, although deposit rates will also follow suit.

From credit cards and mortgage rates to auto loans and savings accounts, here’s a look at where those rates could go in the year ahead.

Credit cards

Going forward, annual percentage rates will start to come down when the Fed cuts rates but even then, they will only ease off extremely high levels. With only a few potential quarter-point cuts on deck, APRs would still be around 20% by the end of 2024, McBride noted.

“The credit card rates are going to mimic what the Fed does,” he said, “and those interest rate decreases are going to be modest.”

Mortgage rates

Due to higher mortgage rates, 2023 was the least affordable homebuying year in at least 11 years, according to a report from real estate company Redfin.

Although 15- and 30-year mortgage rates are fixed, and tied to Treasury yields and the economy, anyone shopping for a new home has lost considerable purchasing power, partly because of inflation and the Fed’s policy moves.

But rates are already significantly lower since hitting 8% in October. Now, the average rate for a 30-year, fixed-rate mortgage is 6.9%, up from 4.4% when the Fed started raising rates in March 2022 and 3.27% at the end of 2021, according to Bankrate.

Doug Duncan, chief economist at Fannie Mae, expects mortgage rates will dip below 6% in 2024 but will not return to their pandemic-era lows, which is little consolation for would-be homebuyers.

“We don’t see the affordability problem solved until supply increases substantially, interest rates come down and real incomes rise,” he said. “The combination of those things need to move together over time. It’s not going to be sudden.”

Auto loans

The average rate on a five-year new car loan is now more than 7%, up from 4% when the Fed started raising rates, according to Edmunds. However, rate cuts from the Fed will take some of the edge off the rising cost of financing a car — possibly bringing rates below 7% — helped in part by competition between lenders and more incentives in the market.

“There are some very encouraging signs as we kick off 2024,” said Jessica Caldwell, Edmunds’ head of insights.

“Incentives are slowly coming back as inventory improves,” she said, and “most consumers are looking for low APRs with longer loan terms, so the growth in those loans is helpful to lure consumers who have been sitting out due to adverse financing and pricing conditions.”

Savings rates

While the central bank has no direct influence on deposit rates, the yields tend to be correlated to changes in the target federal funds rate.

As a result, top-yielding online savings account rates have made significant moves and are now paying more than 5% — the most savers have been able to earn in nearly two decades — up from around 1% in 2022, according to Bankrate.

Although those rates have likely maxed out, “it will be another good year for savers even if we do see rates come down,” McBride said. According to his forecast, the highest-yielding offers on the market will still be at 4.45% by year-end.

Now is the time to lock in certificates of deposit, especially maturities longer than one year, he advised. “CD yields have peaked and have begun to pull back so there is no advantage to waiting.”

Currently, one-year CDs are averaging 1.75% but top-yielding CD rates pay over 5%, as good or better than a high-yield savings account.

Subscribe to CNBC on YouTube.

Don’t miss these stories from CNBC PRO: